How Open Banking and Open Finance Are Transforming Financial Services

A Strategic Guide for FinTechs & Embedded Banking Executives

The era of siloed financial data is coming to an end.

With the rise of open banking, open finance and data-sharing frameworks, banks, fintechs and embedded finance platforms are unlocking new ways to deliver value, personalize services and create competitive advantage.

In this guide, we’ll explore:

What open banking really means;

Survey the current state both in the U.S. and internationally;

Highlight the most promising use-cases;

Provide a comparative vendor landscape for U.S. players, and

Forecast key trends heading into 2026.

If you're in fintech, a B2B SaaS provider, founder or banking executive, this is your strategic primer for the next wave of data-driven financial innovation.

What is Open Banking?

Open banking is often touted as a disruptive regulatory and technological shift, but what does it truly mean for financial services?

At its core, open banking refers to the secure, consumer-consented sharing of financial account data (and increasingly payment initiation) via standardized application programming interfaces (APIs).

This enables third-party providers (TPPs) to access a consumer’s banking data (with permission) and deliver services such as account aggregation, payment initiation, credential-less transfers, credit evaluation, and more.

More broadly, the concept extends into “open finance” (data sharing across savings, investments, pensions, insurance) and ultimately “open data” frameworks where financial, social and other data sets converge.

Key Features & Enablers

Customer consent and control: The individual grants permission for data to flow. Without a robust consent mechanism, the model fails.

Standardized APIs and data formats: To enable scale across institutions and third parties.

Real-time or near-real-time data access: Rather than traditional batch feeds or statements.

Security, identity and fraud controls: Because moving sensitive financial data and payments mandates strong safeguards.

Business and regulatory model alignment: A sustainable ecosystem demands that banks, fintechs, and regulators align incentives and frameworks.

Why It Matters

Open banking unlocks the value of previously locked-up data assets and enables new business models.

Banks can monetize data, improve product cross-sell, personalize services, and reduce costs (e.g., in credit underwriting or KYC).

Fintechs can innovate faster by tapping into ready-built infrastructure rather than building every connection.

Ultimately, for consumers and businesses it means more control, choice, efficiency and tailored experiences.

The transformation from “open banking” to “open finance” marks the shift from bank-centric to platform/data-centric ecosystems.

In short, open banking is the foundational infrastructure layer of a new financial data economy. With consent, APIs and standardization, financial services firms can unlock new value chains and deliver--on the promise of more inclusive, efficient and personalised financial experiences.

In the next sections we’ll explore how this is playing out in the U.S. and abroad, and what use-cases are gaining traction now.

Current State of Open Banking — U.S.

The U.S. open banking landscape is in flux.

Unlike the European Union’s clear regulatory mandate under PSD2, the U.S. lacks a unified federal open banking regime.

Instead, data sharing has developed via bilateral agreements, industry initiatives, and regulatory expectations under development.

Recent developments, however, signal that a shift may be underway.

Regulatory & Market Landscape

In October 2024 Consumer Financial Protection Bureau (CFPB) finalized a “personal financial data rights” rule under Section 1033 of the Dodd‑Frank Wall Street Reform and Consumer Protection Act, signaling a potential federal open banking standard.

But as of 2025 the rule has been stayed and the CFPB has initiated a substantial rewrite of its approach. For example, a federal judge in Kentucky granted a stay on compliance dates pending new rule-making.

Meanwhile, in October 2025 the CFPB opened a 60-day comment period during which roughly 13,900 filings were submitted over data access, API standardization and bank/fintech roles.

Critically, banks are pushing back: some forced fintechs paying for access to data, while others pursue bilateral deals.

For example JPMorgan Chase & Co. indicated that it would charge fintechs for access to account-data unless the regulatory regime is clarified.

Adoption & Market Realities

From the fintech perspective, open banking in the U.S. remains less mature than key global markets.

The lack of mandated PIS/AIS frameworks, inconsistent standards and fragmentation mean many fintechs rely on data-aggregation/screen-scrape models or negotiated access rather than standardized APIs.

Nevertheless, there is momentum: consumer acceptance of bank innovation is strong — 86% of Americans say innovation and technology improvements by banks are making it easier to access financial services.

And the industry standard-setting body Financial Data Exchange (FDX) has reported growing adoption of its API standard (FDX API) with over 53 million consumer accounts and counting.

Key Challenges

Regulatory uncertainty: The U.S. open banking rule is under review and dates are unclear. Fintechs and banks face ambiguity which slows investment and roll-out.

Inconsistent bank participation and fees: Without mandated frameworks, banks have discretion over access, pricing, format and terms (e.g., JPMorgan’s negotiating fees).

Standardization gaps: Data formats, API protocols and consent mechanisms vary widely, increasing integration friction.

Legacy infrastructure & security risk: Financial institutions must upgrade systems and ensure robust security/fraud controls before enabling third-party access.

In the U.S., open banking is at a turning point.

The regulatory framework is under revision, market participants are jostling for advantage, and the underlying infrastructure is being built.

For fintechs and B2B SaaS companies focused on innovation in banking, the next 12–18 months will be critical: those who position now will capture the early-mover advantage as standards coalesce.

Current State of Open Banking — International

Outside the U.S., many jurisdictions have taken more proactive regulatory and infrastructural approaches to open banking and open finance, making them useful benchmarks for what the U.S. may aim to emulate.

Europe & UK

The European Union’s Revised Payment Services Directive (PSD2) (effective from 2018) mandated banks to open APIs to licensed Third-Party Providers (TPPs) for Account Information Services (AIS) and Payment Initiation Services (PIS).

The UK’s regulator similarly implemented open banking frameworks.

Asia & Other Regions

Many markets in Asia-Pacific (Singapore, Australia), Latin America (Mexico, Brazil) and Africa are now actively developing open banking frameworks.

For instance, Mexico’s Fintech Law of 2018 includes provisions for data sharing and open banking.

According to a cross-country study, open banking enables consumers to share transaction data with both banks and fintechs; evidence shows 49 countries have open banking frameworks or initiatives underway.

Maturity Comparison

Regulation-led adoption: Many jurisdictions mandate data access rights, third-party registration/licensing, standard API frameworks and defined roles for banks/fintechs.

Infrastructure & standardization: Europe has made more progress in aligning definitions, APIs, consent models and transaction data enrichment. For example, open finance efforts look beyond banking into assets/insurance.

Use-case diversity: International markets are deploying open banking data for credit-scoring, real-time payments, small-business cash-flow insights, wealth management and embedded finance at scale.

Lessons for the U.S.

Regulatory clarity accelerates adoption: Where governments require banks to expose data via standard APIs, fintech innovation accelerates.

Data normalization matters: Aggregation across banks is surprisingly complex due to terminology and format differences — in open finance this problem multiplies.

Embedded finance and open data converge: Markets abroad show that open banking is a stepping-stone to open finance, consumer data ecosystems, and embedded banking models.

Global competition: Fintechs operating across borders will favor jurisdictions with clearer, standardized frameworks — making U.S. inaction a strategic risk.

Globally, open banking is evolving rapidly and has already moved beyond banking into open finance, real-time payments, and embedded services.

For U.S. fintechs and SaaS players, the international experience offers a roadmap — and a warning: those who wait risk falling behind international peers.

Top Use Cases for Open Banking & Open Finance

Now that we’ve established the landscape, it’s time to dig into the high-value use cases that drive ROI from open banking and open finance initiatives.

These are the business models and execution opportunities where fintechs, banks, or enterprise platforms can capture advantage.

1. Creditworthiness, Underwriting & Risk Management

Open banking enables lenders and financial institutions to move from static credit bureau data to real-time, permissioned access to consumers’ transaction history, income and cash-flow.

In France and Spain, adoption in automated lending (larger/higher-risk loans) is fueled by open-finance data.

Benefits: faster decisions, fewer manual steps, better risk-pricing and more inclusive access for underserved borrowers.

Challenges: ensuring data quality, normalization across banks, avoiding proxies that may create bias or unfair discrimination.

2. KYC, Fraud Management & Identity Verification

Open banking data can be used for instant account verification, transaction history analysis, income/expense verification and fraud-detection workflows. Combined benefits of open banking are building momentum for open finance.

Benefits: reduced onboarding friction, better AML/KYC compliance, lower fraud losses, improved customer experience.

Challenges: privacy concerns, regulatory oversight, building composable fraud-detection models that consume this data safely.

3. Embedded Finance & Verticalized Platforms

Open banking enables financial capabilities to be embedded into non-financial platforms (ERPs, accounting software, marketplaces) thanks to data access and payment initiation.

Open finance is a key enabler for embedded finance: real-time access to balances, cash-flow and data enables non-banks to integrate financial services seamlessly.

Examples: A SaaS-business-platform embedding payments, lending, treasury, financing based on cash-flow drawn from aggregated account data.

Benefits: new revenue streams, deeper customer engagement, platform expansion beyond core offering.

Challenges: building trust with end-customers, orchestration across partners, liability management.

4. Personal Finance, Wealth & Advice – Data-Driven Insights

The expansion into open finance allows aggregating savings, pensions, investment, insurance and banking data — enabling wealth managers and fintechs to deliver hyper-personalized financial advice.

Wealth managers use open finance data to shift from standardized products to personalized services.

Benefits: stronger customer value, higher retention, new product cross-sell.

Challenges: data normalization, consent renewal, regulatory protections around advice.

5. Real-Time Payments & Account-to-Account (A2A) Transfers

Open banking payment initiation services (PIS) enable direct bank-to-bank transfers, bypassing cards and reducing costs.

While adoption is more advanced abroad, U.S. initiatives tied to instant payments are gaining traction. t

Benefits: lower interchange, better user experience, new fintech opportunities (financed checkout, merchant tools).

Challenges: bank adoption, standardization of APIs, coordination across networks.

6. Financial Inclusion & Alternative Data

For under-banked or thin-credit-file consumers, open banking data provides alternative signals (cash-flow, rent payments, utility payments) to build profiles. This becomes impactful for improving finance accessibility in developing markets.

Benefits: expanded addressable market, social impact, new growth.

Challenges: fairness of algorithms, data bias, regulatory oversight.

These use-cases illustrate how open banking and open finance unlock real operational and strategic value across credit, payments, embedded finance, wealth tech and inclusion.

For fintechs and B2B SaaS platforms, the key is aligning the value proposition with one or more of these models — and selecting partners/vendors that accelerate time-to-market.

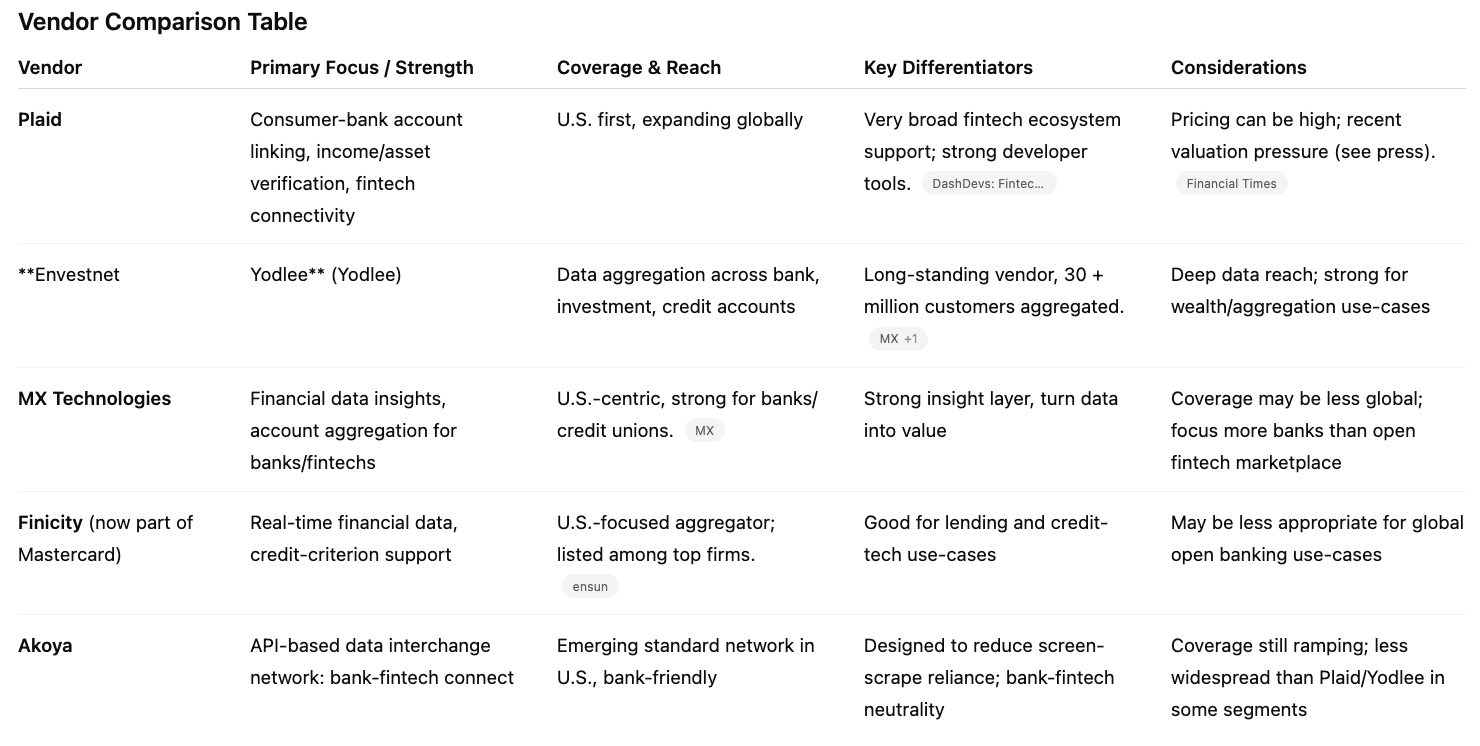

Top Open Banking Vendors in the U.S. — Comparative Evaluation

If you’re a fintech or B2B SaaS company exploring open banking data, selecting the right vendor partner is critical.

Below is a comparative overview of leading U.S. open banking/data-aggregation vendors and how they stack up across important dimensions (coverage, API maturity, fintech-friendliness, pricing, strategic fit).

This will help you make a quick evaluation and prioritise shortlist candidates.

Vendor Comparison Table

How to Choose the Right Vendor – Key Criteria

API coverage & bank connectivity: How many bank/institution endpoints, real-time access, reliability.

Regulatory readiness & consent management: Does the vendor support secure, auditable consent flows, compliance with forthcoming U.S. standards?

Data normalisation & enrichment: The value of aggregated data depends on consistent formatting, classification & enrichment.

Fintech platform friendliness / developer experience: Quality of sandbox, SDKs, documentation, ease of integration.

Pricing and business model alignment: Understand vendor pricing tiers (data-volume, API calls) and align with your business model.

Strategic fit with use-case: Some vendors are stronger for lending use-cases (Finicity), others for broad consumer linking (Plaid), others for bank-centric insight (MX).

Future-proofing — global expansion & open finance readiness: If you target more than U.S., look for vendor capability for multi-jurisdiction / open finance expansions.

Quick Evaluation Summary

If your target is fast consumer-fintech linking (budgeting apps, payments), Plaid is a strong choice.

If your focus is lending and credit underwriting, Finicity (or Yodlee) may provide richer historical insight.

For bank/credit-union partnerships (white-label data insights), MX stands out.

For bank-fintech connectivity with neutral interchange (avoiding screen-scrape), Akoya is worth watching for the U.S. standard.

If you expect to expand globally (or into open finance beyond banking), evaluate vendor global reach and whether they support “beyond-bank” datasets (investments, pensions).

Selecting the right open banking vendor is a strategic decision — not just a technical one.

For embedded banking or fintech services, the right partner can accelerate GTM, reduce time-to-value, and provide a competitive moat.

Use the criteria above to benchmark vendors and align with your specific use-case and geographic ambition.

Upcoming Trends & What to Watch in 2026

As we look ahead to 2026, several trends in open banking and open finance will reshape strategic planning for fintechs, banks and embedded-finance platforms alike.

Being ahead of the curve will distinguish winners from laggards.

Trend 1: The Rise of Open Finance & Data Ecosystems

Open banking is the stepping-stone.

The next frontier is open finance (broadening beyond transaction accounts to savings, pensions, insurance, mortgages and investment data) and eventually open data (including social, behavioral, and non-financial data).

Implication: Fintechs that build platforms capable of ingesting and leveraging cross-vertical data (e.g., bank + pension + insurance) will deliver differentiated value.

Trend 2: Embedded Finance Meets Data Monetization

Embedded finance is accelerating — e.g., B2B platforms embedding lending, payments, bank accounts.

Open banking/data provides the connective tissue for that. Embedded finance and open banking are intimately connected.

Simultaneously, banks and data platforms will seek to monetize data access, refinement and services. For example, U.S. banks negotiating data-access fees signal this monetization pressure.

For 2026: expect more bank-fintech revenue-share models, “data-as-a-service” partnerships, verticalised embedded finance offers tied to data insights.

Trend 3: Regulatory & Standardization Momentum in U.S.

The U.S. regulatory environment, while delayed, is moving. The CFPB dive brief indicates “the consumer-data-rights rule arguably marked a milestone … recognizing secure APIs as the foundation for permissioned data flows.”

With the rule being reconsidered, for 2026 we should see clearer mandates: e.g., defined roles for banks/TPPs, API standards, pricing frameworks, consumer rights enforcement.

For fintechs: being prepared for compliance (consent, security, auditability) will be table-stakes in 2026.

Trend 4: Data Normalization, Enrichment & AI/ML-Driven Insights

Having access to data is not enough; enriching, standardizing and making it actionable is where the real value lies.

Meanwhile, academic research on open banking shows foundational-model approaches to transaction data (masking, representation, sequence modeling) are emerging.

For 2026: fintechs that invest in enriched data layers, build ML/AI driven insights (cash-flow forecasting, anomaly detection, segmentation) will differentiate.

Trend 5: Ecosystem Expansion — Real-Time, Cross-Border, Inclusivity

Real-Time & A2A Payments: Open banking enables faster transfers, lower-cost payments and richer experiences. The International overview shows progress.

Cross-Border/Open Regional Models: As embedded finance scales globally, data APIs will need to support multi-jurisdiction access, multi-currency, multi-reg sets.

Inclusivity & Alternative-Data Models: With inflation, underwriting stress and thin-file populations, open banking/inclusion models (non-traditional data) will gain traction.

Trend 6: Data Governance, Ethics & Consumer Trust

As more personal financial data flows through multiple parties, governance, ethics and security become central.

Research warns about “hidden implications for fairness,” as transaction data may inadvertently proxy for protected attributes.

In 2026, consumers will expect transparency on how their data is used, stronger audit trails, clearer opt-in/opt-out models and fintechs will need to embed “trust” into their data products as a differentiator.

For fintechs and embedded-banking platforms, 2026 will not be about “if” open banking/data will matter — it will be about “how” you integrate, monetize and scale it.

The winners will be those who build data-rich, insight-driven, compliant platforms that leverage open banking as a springboard into open finance, embedded services and global scale. Start positioning now.

Strategic Action Plan for FinTechs & B2B SaaS Companies

This section offers a high-level roadmap for how you, as a fintech, embedded-banking platform or B2B SaaS vendor, can capitalize on open banking/data trends in 2025-26.

1. Define Your Use-Case & Value Proposition

Select one or two core use-cases (e.g., lending, embedded payments, wealth aggregation, data-driven SME cash-flow management) where open banking data unlocks visible value.

Flesh out the business model: what data you need, what value you will deliver, how you monetize it and how you differentiate.

Align with vendor capabilities (see vendor comparison above) and ensure the partner ecosystem supports your GTM.

2. Build Data Strategy & Architecture

Define data ingestion strategy: which banks/institutions, what data types (transaction, investment, pension, insurance).

Ensure robust consent flows, API reliability, data normalisation, enrichment and analytics layer.

Build for scale: assume real-time or near real-time, high volume, multi-jurisdiction in future.

3. Choose Vendor(s) & Infrastructure

Use the comparative framework above to select primary data-partner(s). Consider multi-vendor for redundancy or diversification.

Negotiate favourable pricing, clear SLAs, developer support, sandbox access and alignment with your use-case.

Build internal dev team or partner with integration experts to ensure smooth roll-out.

4. Regulatory & Compliance Readiness

U.S.: monitor the CFPB rule-making process and build compliance readiness (consent logs, audit trails, data usage policies, vendor management).

Globally: if you have cross-border ambitions, map out region-specific open banking/open finance frameworks now.

Embed data-governance, privacy and ethics into your operating model.

5. Go-to-Market & Scale Strategy

Launch minimum-viable product (MVP) with core functionality and proof-points (e.g., faster credit decisions, embedded payments, improved conversion).

Use case studies, metric-driven results and customer success to scale.

Expand verticals and geographies: step into “open finance” data sets (pension, investment, insurance) as your foundation grows.

Monitor ecosystem dynamics: vendor-bank relationships, pricing models, regulatory shifts (e.g., banks charging data fees) and competitor moves.

6. Measure ROI & Iterate

Key performance indicators (KPIs): reduction in underwriting time, conversion lift, cost-to-serve, incremental revenue from embedded finance, data monetisation margin.

Use dashboards to monitor vendor performance (API uptime, data accuracy, enrichment quality).

Iterate your data-stack, add machine learning-driven insights, refine your value proposition.

By aligning your product roadmap with open banking/data infrastructure, choosing the right vendor ecosystem, and building a compliant, scalable architecture, your fintech or B2B SaaS platform can transform from “data-enabled” to “data-driven.”

The race for streamlined banking and platform finance is already underway — position to win.

In closing

The open banking and open finance era is not a distant future — it is happening now.

For financial services firms, fintechs and B2B SaaS platforms, the strategic implications are profound.

From unlocking new credit models and embedding finance into vertical platforms, to leveraging enriched data insights and preparing for global expansion, the opportunities are real.

However, these opportunities come with complexity: regulatory uncertainty (especially in the U.S.), vendor selection risk, data governance mandates and the need for robust infrastructure.

For those in the financial services community, the imperative is clear: act now.

Start with a specific use-case, pick your vendor(s) wisely, build for scale and compliance, and roadmap into 2026 with a view toward open finance, embedded banking and global full-stack data platforms.

As open banking moves from “nice-to-have” to “must-have,” the firms that move early and build infrastructure and partnerships wisely will capture the outsized value.

In this evolving landscape, being data-driven is no longer optional — it’s the pathway to growth, differentiation and long-term resilience.

Call to Action (CTA):

If you’re a fintech or embedded-finance platform exploring open banking/data capabilities, we can help!

Reach out for GTM advisory, vendor research, pipeline strategy or embedded-banking program design. Let’s unlock the data-driven future together!